I am not alone in thinking the current economic environment is getting worse. Inflation remains stubbornly high in most parts of the world, which in turn has forced finance ministries to keep interest rates elevated longer than initially anticipated, which is putting pressure on company earnings. The “AI boom” in the S&P seems to be cooling down, the possibility of an all-out regional war in the Middle East does not seem inconceivable and news agencies across the globe are bemoaning unemployment levels.

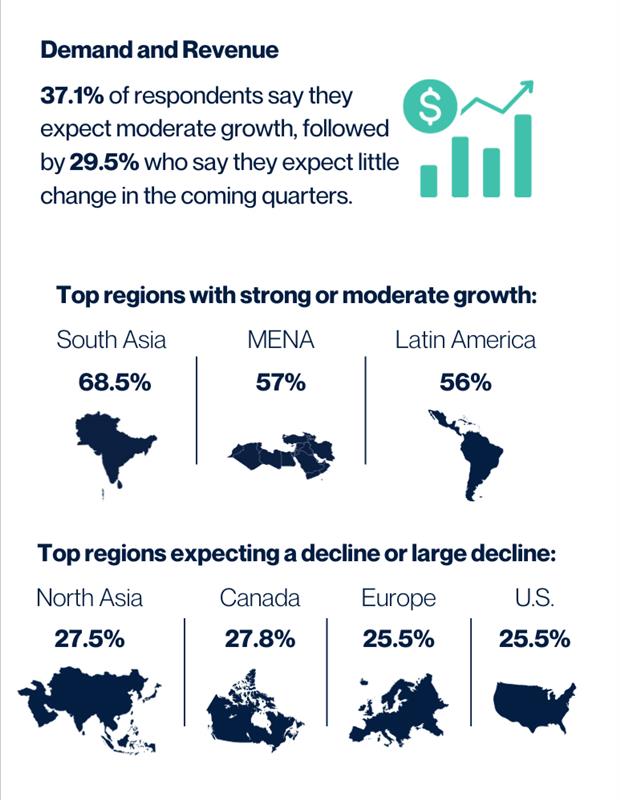

However, reflecting on the data collected from 2,123 CEOs from 108 countries in the latest YPO Global Pulse, there are pockets of the globe that are starting to see the light at the end of a very long and dark tunnel. Leaders with the most positive overall outlook come from South Asia, closely followed by Latin America. This is largely driven by their reporting a greater than 5% increase in both turnover and total fixed investment since last year this time, and is despite their expectation of high inflation and high interest rates.

A significant 57.7% of the South Asia leaders are anticipating that business and economic conditions will be ‘much’ or ‘somewhat’ better in the next six months. Additionally, only 14.1% of South Asian leaders are expecting a recession in their market within the next year. The region’s confidence is underpinned with almost 60% of the respondents believing that sales (turnover) will be up by more than 5% on the prior year. This is further corroborated by 46.6% of respondents planning to increase their fixed investment by more than 5% year-on-year, and 27.1% of the respondents indicating they intend to employ more people this year.

However, despite the optimism felt in South Asia, there’s a looming shadow in the data – the anticipation of a global recession. A significant proportion of the respondents (50.2%) recognize this risk, aligning closely with The Wall Street Journal’s prediction of 48%. Despite this cloud of uncertainty, most respondents believe their businesses can remain viable for more than a decade if they continue their current path. It is encouraging that only 1.9% hold less optimistic expectations, believing their businesses might not last a year.

In regions that have enjoyed low interest rates for an extended period, notably Canada, Europe, North Asia and the U.S., approximately 48% of CEOs are expecting a regional recession and a decline in demands and revenues within the next year. The longer it takes for interest rates to start reverting to their long-term average, the more this negative sentiment is spreading.

—

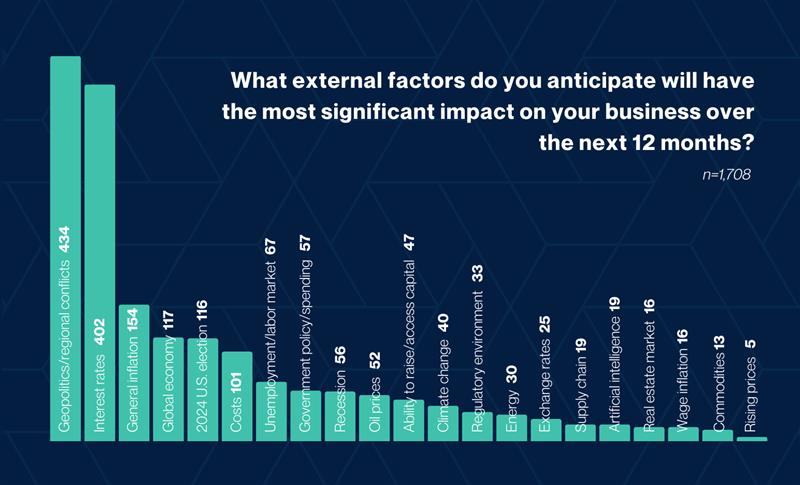

Geopolitics and regional conflicts, alongside economic factors like interest rates and general inflation, are having a significant influence on the way businesses are planning for the coming year. The 2024 U.S. presidential election, costs, unemployment, exchange rates, regulatory environments, and oil and energy prices are all factors. It’s no surprise that some business leaders are struggling to see beyond the potential for a recession. I have become increasingly convinced that Batman was right when he said that it is “darkest just before dawn,” because even with the complex geopolitical and economic headwinds, the data is showing that the environment in which we are all doing business is improving, and although things might get worse in certain areas, on the whole we are moving toward a new era of prosperity.