As the coronavirus contagion slows and countries ease restrictions, business around the globe is gradually reigniting as chief executives express greater levels of optimism according to YPO’s third Chief Executive COVID-19 Global Survey.

Though the majority (64%) of respondents say their business outlook is more negative compared to 1 March, this is a marked improvement from the previous month, when 84% of chief executives had a negative outlook, showing the long road to recovery has begun. Touching base with its global community just six weeks after its second COVID survey, YPO asked its members to provide their one-year outlook for business outcomes, identify obstacles to business viability and report on the pace of reopening in their regions of business. Global leaders also reflected on lessons learned from the past three months navigating the unchartered business disruptions of the pandemic.

More than 2,700 chief executives ages 25-91 in 100 countries provided feedback. Roughly half of the respondents are from the United States.

What’s changed since March?

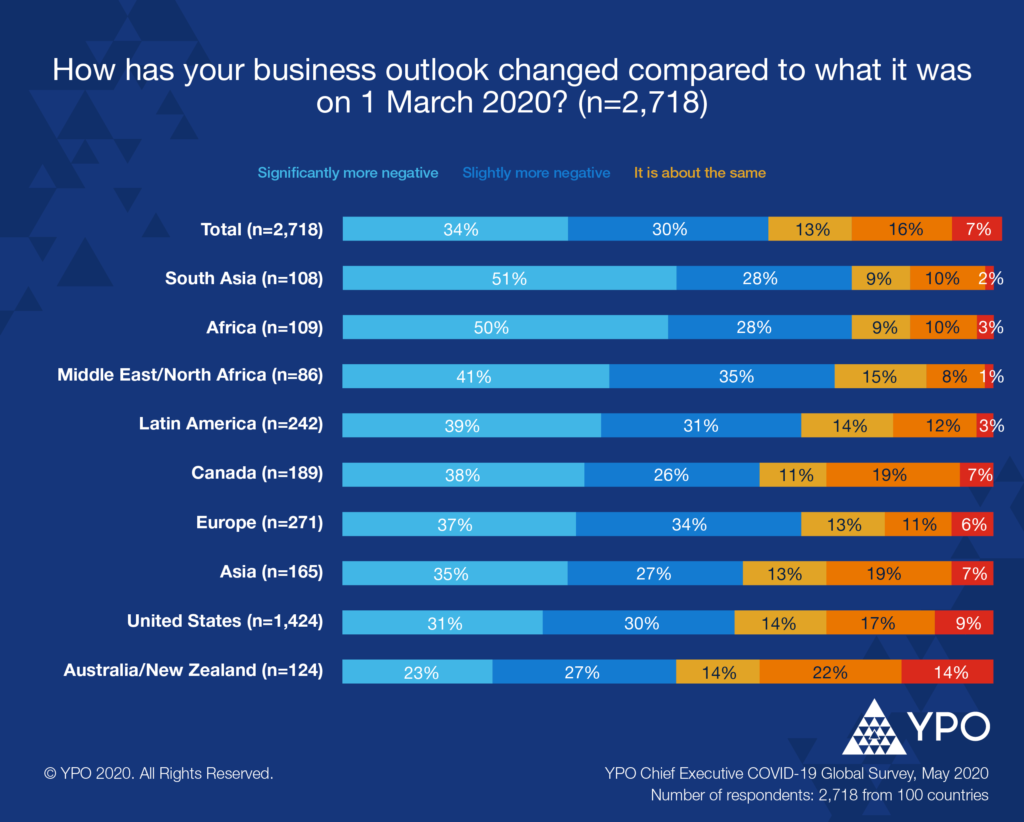

Business outlook shows an increase in optimism among chief executives compared to the YPO April survey, with 23% reporting they are slightly or significantly more positive since 1 March.

As the COVID-19 pandemic progresses, regional differences are emerging. Australia/New Zealand (35%) leaders have the most positive business outlook since March, followed by Canada (26%) and the U.S. (26%). However, executives in South Asia (51%) and Africa (50%) are significantly more likely than their counterparts in Asia (35%), the U.S. (31%) and Australia/New Zealand (23%) to express a more significantly negative outlook since March.

Differences in business outlook are greater between industries as various areas of the world move into the stages of reopening, yet, in every industry, there is a decline in a significantly negative outlook compared to early March between April and May.

Leaders in the hospitality/restaurant (69%), aerospace/aviation (59%) and automotive (45%) industries expressed that their outlook has significantly worsened while executives in telecommunications (52%), health care (35%) and the food and beverage (32%) industries have a more improved outlook. These were the top three sectors with the most positive outlook since April, indicating that business outlook by industry has not significantly changed.

While the majority of responses are still overwhelmingly negative, respondents in the retail and wholesale sales (+12%), automotive (+11%) and aerospace/aviation (+9%) industries had the greatest month-over-month change in becoming significantly more positive about what’s to come.

Shifting to a new phase

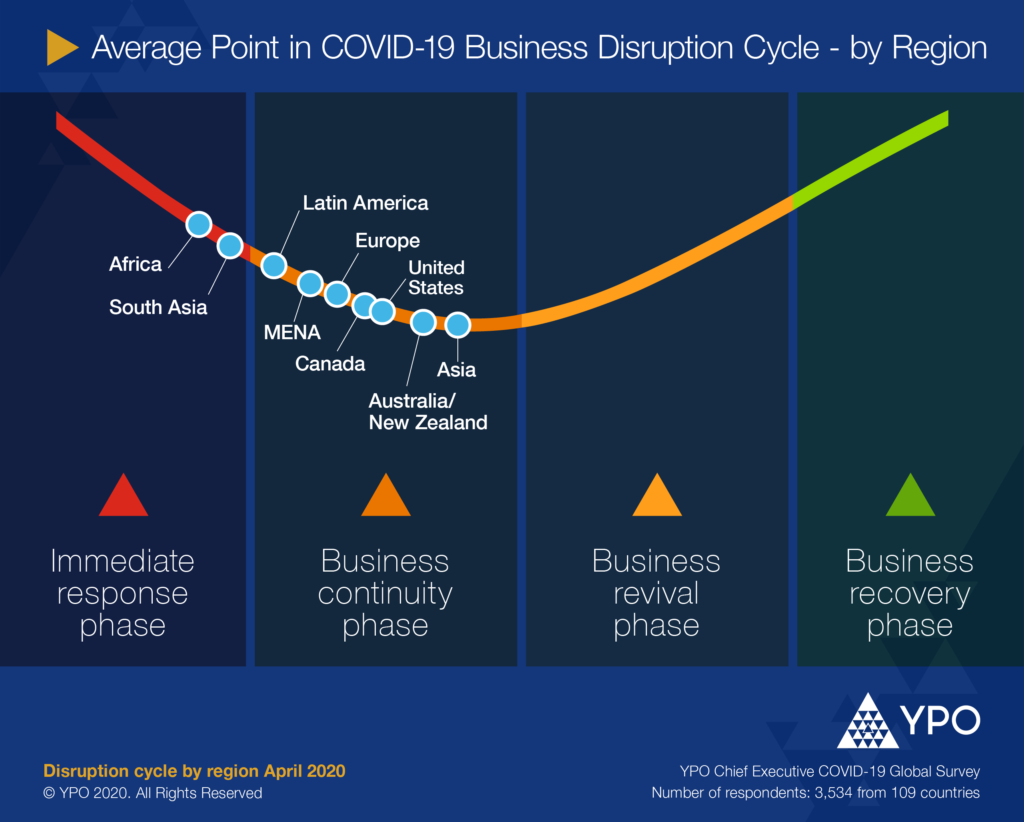

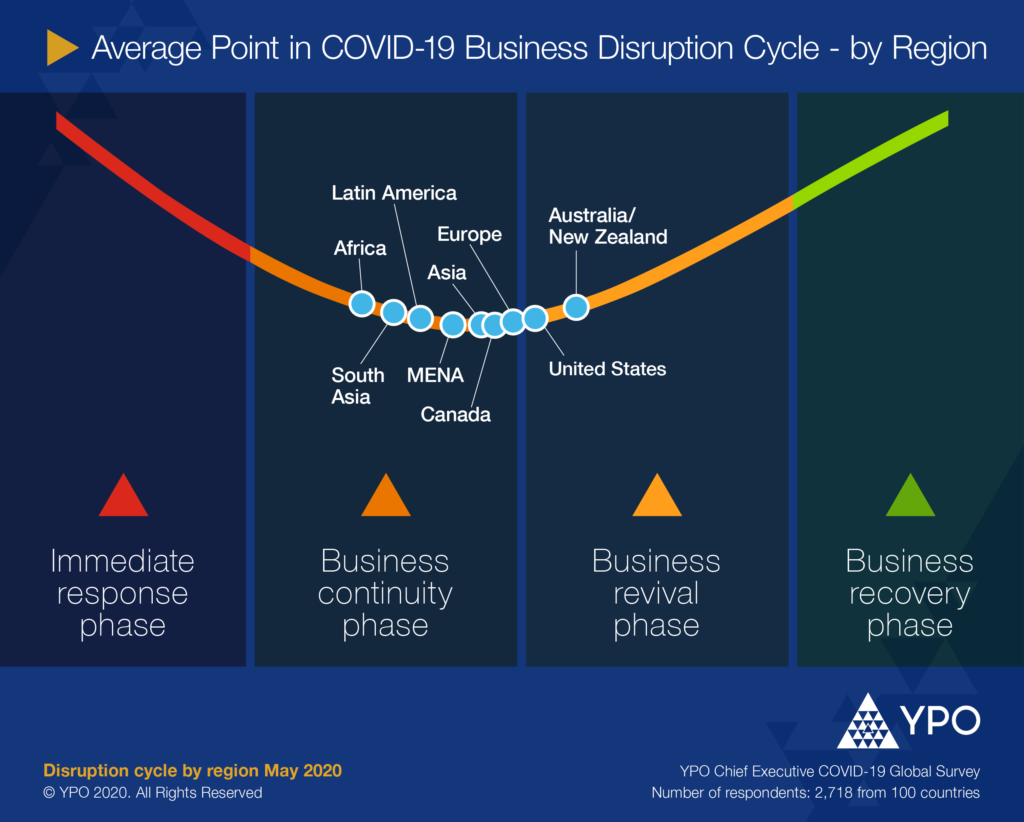

Overall, the YPO survey found that the business world is slowly shifting toward the revival phase, with business activity beginning to resume and the economy on an upward trajectory.

Forty-nine percent of the YPO survey respondents report that they are in the business continuity phase — living through the impact, withstanding economic loss — due to the COVID-19 crisis, and 39% say their country is in the business revival phase, with leaders in Australia/New Zealand and the U.S., on average, being furthest along in the business disruption cycle.

Africa business leaders report that they are in the earliest response stage on average, followed by South Asia. Since March, Asia has experienced the smallest movement along the business disruption cycle month-over-month.

In terms of industry, the greatest progress along the business disruption cycle between April and May is health care, and the industries that progressed the least are hospitality/restaurant and real estate.

What’s the outlook?

Sentiment was clear from chief executives surveyed that a prolonged recovery is expected. Almost half (48%) anticipate continuing negative effects on revenues one year from now as compared to March levels. They also foresee similar effects on total number of employees and total fixed investment with 39% expecting both the total number of employees and total fixed investment to still be down by at least 10% a year from now.

Executives forecast increases of at least 10% in revenues (27%), followed by fixed investments (21%), then headcount (15%). These increases exceeded those in April and March survey data, reinforcing the sentiment that leaders have growing optimism about business incomes.

Generally, survey data indicates a shift across industries toward more optimistic sentiments regarding revenue as compared to April responses, with no significant increase in pessimism in any industry.

Obstacles to business viability

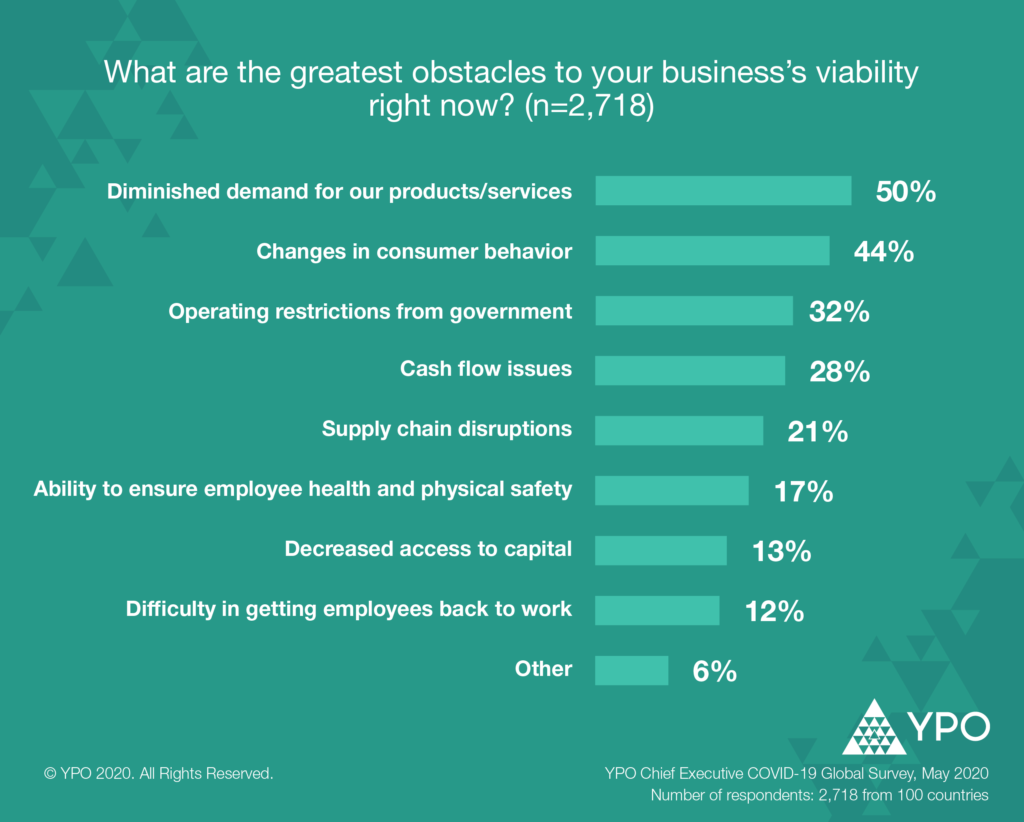

Half of chief executives say the greatest threat to business recovery right now is shrinking consumer demand (50%), changing consumer behavior (44%) and operating restrictions from government (32%), according to the YPO survey.

Leaders in the U.S., South Asia and Africa face the following obstacles more so than other regions:

- Ability to ensure employee health and safety 20% (U.S.)

- Difficulty in getting employees back to work 29% (South Asia)

- Cash flow issues 54% (Africa)

Ready for business

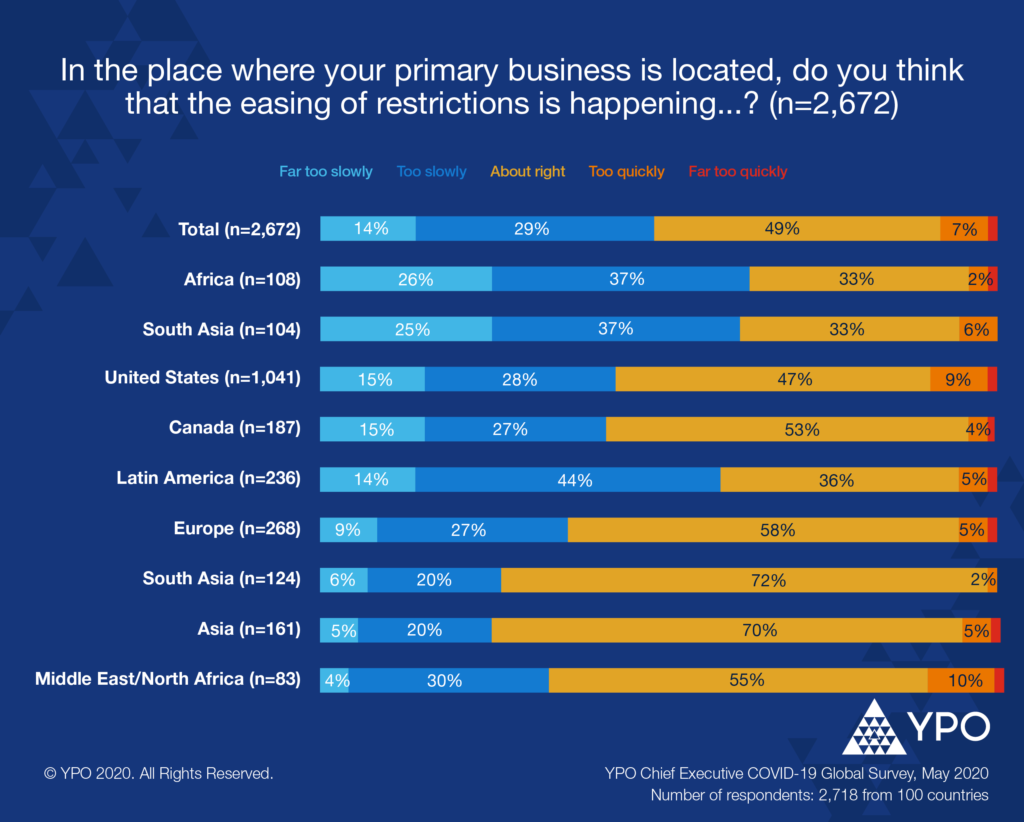

Is it time to get back to business? Business leaders are split (49%) when it comes to easing restrictions and reopening at a pace that is about right, whereas 29% feel their region is reopening too slowly. Of those who expressed that reopening is occurring too slowly, 52% operate their business in a place where some non-essential businesses are open with restrictions.

Africa, South Asia and Latin America chief executives expressed that their countries are easing restrictions far too slowly. Middle East/North Africa chief executives are most likely to say reopening is happening too quickly (11%) followed by the U.S. (10%).

Relief

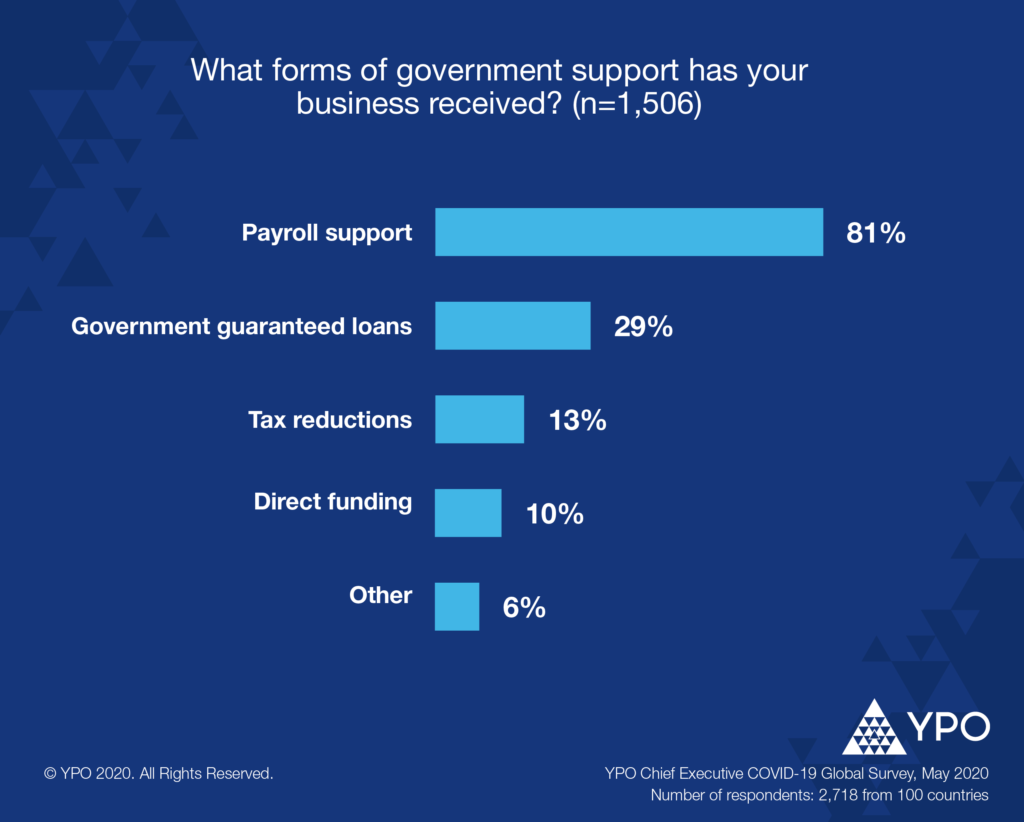

Overall, 55% of survey respondents report that they received some form of support from the government during the pandemic. Of those receiving support, 81% came in the form of payroll support, and 29% came from government-guaranteed loans. Of the 45% who did not receive government support, most (44%) cited that their business does not require it.

Can we withstand a second wave?

If COVID-19 were to see a resurgence in the next few months, 6% of those surveyed say their business would be at risk of not surviving, and 72% say it would post a moderate-to-large threat. Most say that a second wave would be a moderate (36%) to large (36%) threat to their business.

Regional outlooks show that executives in Africa (17%) are significantly more likely than those in Europe (8%), Asia (6%), Canada (6%) and the U.S. (5%) to say a significant resurgence of COVID cases would be a severe threat to their business.

Industries most at risk include hospitality/restaurant, media/entertainment, production (agriculture, chemicals, mines, utilities), retail and wholesale sales and automotive.

What we’ve learned

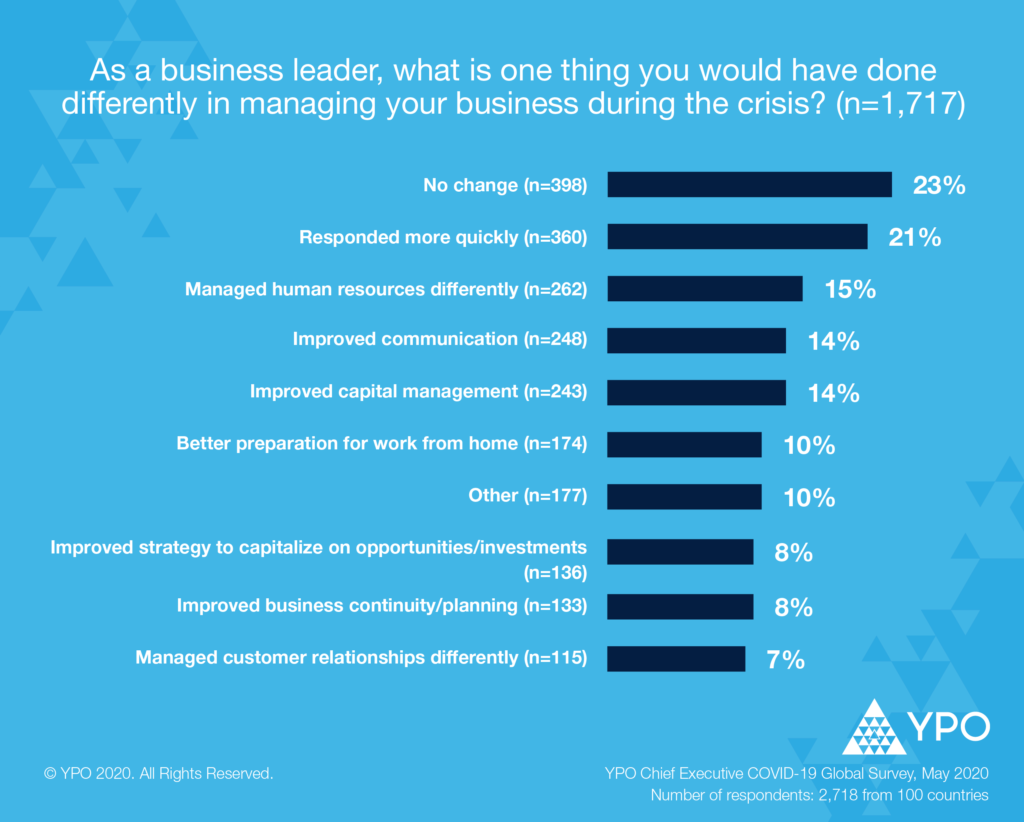

With COVID-19 not likely be the last pandemic in our deeply interconnected world, business leaders were asked how they would handle the crises differently. Survey respondents shared that 23% would not change their leadership approach, while others cited they would be quicker to respond procuring personal protective equipment (21%), manage human resources differently (15%), improve communications (14%) and improve capital management (14%).

For more crisis leadership stories like these, check out the COVID-19: Leading Through Crisis page on YPO.org. All YPO members can find breaking news, offer insights and view current discussions happening about COVID-19 impact within the YPO community on the YPO member-only platform.